Do contractors need to find a huge deposit for a mortgage?

A contractor needs no more deposit than any other homebuyer

It’s a common misconception that contractors need bigger deposits than salaried employees. They don’t! With a genuine contractor mortgage, lenders treat them like any homebuyer.

It’s not difficult to understand where this myth originated, though.

The good and the bad of self-cert mortgages

Before the credit crunch, many contractors used self-cert mortgages to buy a home. As the only proof of income needed for these was self-certified, interest rates were high.

The best way for a contractor to reduce the interest rate was to put down a bigger deposit. With a bigger mortgage deposit, they presented less risk.

So guess what? Word soon spread that contractors needed a bigger deposit for a decent mortgage.

And when people are desperate to believe, they’ll often overlook the facts…

…although, there is an element of truth in that old myth:

How to make your mortgage deposit work harder for you

After years in the wilderness after the credit crunch, 5% deposit mortgages are back. The government’s Help-to-Buy initiative was the catalyst for 95% LTV mortgages returning.

And while 5% is the least you need, you shouldn’t see that as entry level if you can afford more.

The larger the deposit you can find, the lower the interest rate will be on the balance. Today, 15% deposit will secure contractors a respectable interest rate with many lenders.

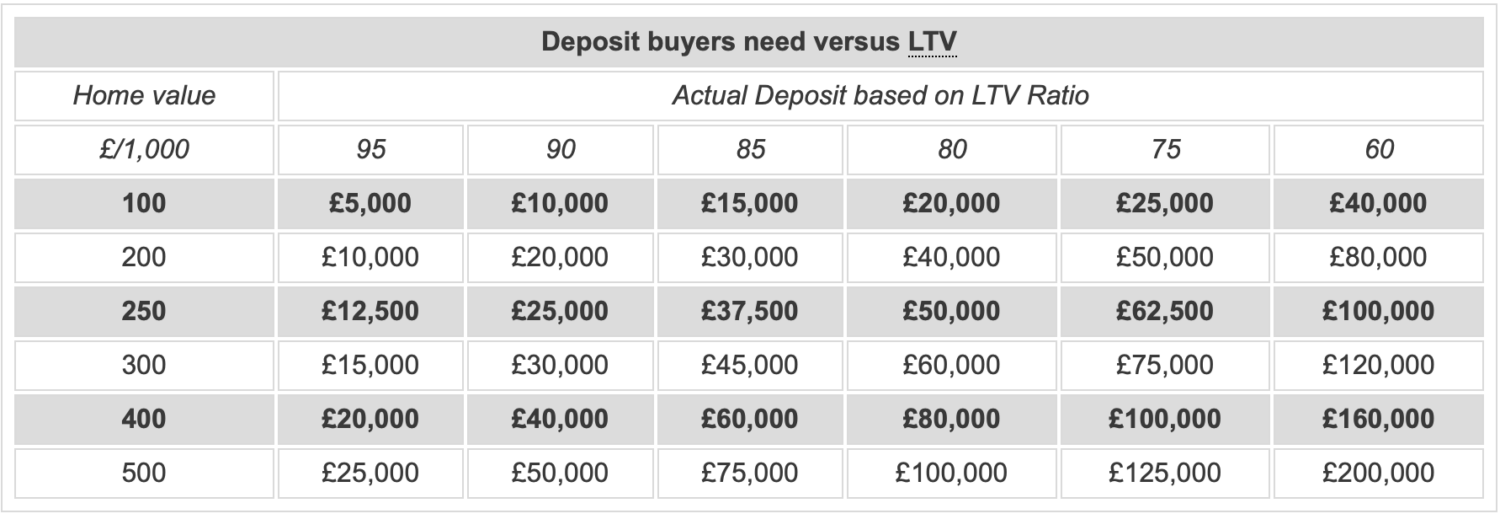

What does LTV – or “loan-to-value” – mean?

LTV is a financial ratio. It signifies a borrower’s loan amount compared to the value of the asset they’re buying.

For mortgages, the difference between the two figures is the deposit.

To qualify for 95% Loan-To-Value mortgages, borrowers need 5% deposit. Thus, 95% + 5% = 100% of the purchased asset price.

Here’s a table that gives examples of LTV versus deposit against property values:

Why use a broker, even if I have more to put down?

Using a specialist broker will help lenders understand your contract income. If you go direct to a local branch, advisers may struggle with your limited company accounts.

Lenders also expect a perfect credit history to reduce risk further. Anything less may well affect the interest rate they offer.

In some cases, an adviser may reject you outright, irrespective of the size of your deposit. A specialist broker can help you choose the right lender for your situation.