Are there any upfront mortgage fees/hidden costs involved?

A quick budget guide to upfront costs and mortgage fees

Besides their deposit, all homebuyers should budget for other mortgage-associated fees. Some you’ll pay at every lender you approach. Others either do not charge or waive, based on your mortgage application.

Some fees are non-refundable, meaning you’ll lose your money if the sale falls through. Others you can choose to add to the mortgage itself and pay over its term. Yet others are service fees, more like a fixed cost than a fee.

Mortgage fees, what they mean and a guide to costs

Your adviser must provide documentation showing all the mortgage fees you’ll incur. This is your “Mortgage Illustration” document, issued when they recommend your mortgage.

Depending upon the mortgage lender, this will either be a KFI or an ESIS. A KFI is a ‘keyfacts illustration‘, which the ESIS is soon to replace. Some lenders already use the ESIS, or European Standard Information Sheet.

Either way, they contain all the relevant cost information a lender has a legal duty to show you. Our overview of the most usual fees is below. You can find full details on the Money Advice Service website.

Mortgage broker fee

If you use a broker, this is their fee for arranging your mortgage or giving advice. All homebuyers should engage a broker, but especially contractors. Broker fees vary, but average out at £500 per mortgage. As many brokers have whole market access, you can easily recoup this fee through the extra choice they offer.

Some mortgage brokers work on the commission they get from a lender alone. A broker’s percentage will depend on their deal with the lender and the mortgage value.

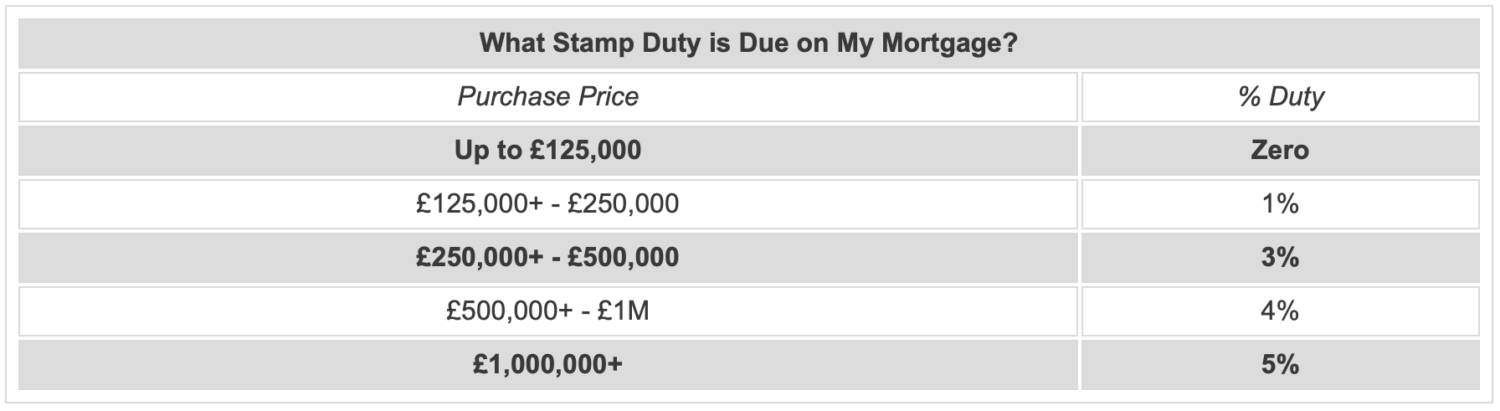

Stamp Duty – calculator and rates

The value of the home you buy dictates if you’ll pay †stamp duty. Our Stamp Duty Calculator page has detailed information about Stamp Duty Land Tax. The latest rates for UK Stamp Duty are:

Stamp Duty for first time buyers and second residences

The rules are different for first time buyers and second homes.

First time buyers can claim a relief discount and pay no Stamp Duty up to £300,000. On any property costing between £300,000 and £500,000, they’ll pay 5%.

If their first home is >£500k, HMRC treats them as a homebuyer who’s bought a home before. The first time buyer then forfeits the right to that discount.

Many contractors invest in buy-to-let properties. There is no additional cost on second homes if they’re <£40,000. If the value is >£40,000 owners pay 3% above current rates.

Provider’s valuation fee

Mortgage lenders have to protect their interests, so value your property. This fee covers that evaluation.

The value of the home has to at least match the mortgage you’re borrowing against it. In certain circumstances, lenders may choose to waive the fee altogether.

There’s also nothing stopping you paying for your own survey too, to add peace of mind. Expect to pay anything between £150-£1,500, either yourself or through your lender.

Arrangement fee

This fee is what you might pay for the mortgage itself. Some lenders may call it the product- or completion fee. It can be free if the lender waives it or cost as much as £2,000.

Often, homebuyers lump this onto the mortgage itself. However, by doing so, they pay interest on the Arrangement Fee for the life of the mortgage.

Mortgage account fee

The lender has to create, manage and close your mortgage account over the term. The mortgage account fee covers those administration costs.

This fee may not cover the cost of redeeming your mortgage before the end of its term. Redemption could kick in when you either pay off the loan early or remortgage.

The £100-300 you pay for lenders’ admin should negate any exit fee, though.

Exit/Closure fee

You pay your Exit fee when you repay your mortgage. It may still apply if you run with your mortgage to the end of its term.

Check your KFI/ESIS, though. Your lender may include Exit costs in the mortgage account fee. The cost alone is between £75-£300.

Early mortgage repayment charges

Lenders’ interest rates assume you’re going to repay a mortgage over the agreed term. If you repay all or part of your mortgage early, it breaks that original agreement.

Some lenders may not charge the fee, especially if you’re remortgaging with them. Others may charge any discounts, cashback or rewards back to your account if you repay early.

Again, check your KFI/ESIS when it’s issued to you if you plan to overpay. The fee could be as much as 5% of the early repayment amount.

Missed mortgage repayment(s)

Each lender decides their own policy on missed payment charges. All adhere to FCA policy, but do check your KFI/ESIS for what they are. Even if they don’t charge, missed payments will accrue interest over the term.

Most lenders are brilliant at helping you get back on track after hiccups. However, the lender could repossess your home if you fail to maintain your repayments.

Mortgage provider higher lending charge

Mortgage underwriting is all about risk. If you only have a small deposit, lenders may insure against potential loss. Negative equity is the big risk. It could see lenders lose money if they have to repossess your property and resell it.

It’s up to the lender to charge it and not all do. If they do, it’s around 1.5% of the mortgage value.

Miscellaneous fees

Smaller fees that, if you’re on a tight budget, soon mount to a sizeable chunk:

Telegraphic transfer fee

Telegraphic transfer is a non-refundable one-off fee from the mortgage provider. It facilitates the transfer of the mortgage pot across the chain. First from the lender to your solicitor, who’ll forward it onto the vendor’s solicitor. Expect to pay £25-£50 for the privilege.

Mortgage booking fee

Some lenders charge a booking fee as soon as you apply for a mortgage. (Not all do.)

It’s a non-refundable payment of between £99-£250. You won’t get your money back even if you’re unsuccessful or your mortgage falls through.

Other lenders charge it with discretion, based on the amount you apply for. Yet others include it in the Arrangement Fee.

Freedom of Agency fee

Some lenders still charge you if you decide to take out your own buildings insurance. It’s a hangover from when lenders guaranteed selling you insurance with your mortgage.

Today, it’s often worth paying the £25 and getting your own. But do check the insurance they offer; it may be competitive.

*Solicitor/Conveyance/Legal fees

Most homebuyers appoint a solicitor to handle the legal side of moving home. Your adviser or broker can often suggest one or you can find a local one yourself.

They’ll deal with your mortgage lender, vendor’s solicitor and action your legal documents. Budget anywhere between £850-£1,500 for this service.

If you’ve got room in the budget, consider asking them to carry out local searches, too. This can turn up any hidden surprises in the locale or planned local construction. Prices range from £250-£300.

*Surveyor’s fee

The lender carries out a basic survey of the property against which the mortgage is secured. This is to ensure that the home you’re buying is worth what you’re borrowing. Depending on the type or age of the home, you may want to instruct a survey of your own.

According to the RICS, only 20% of homebuyers carry out their own survey. The Institute lists several respective surveys to suit different types of home:

Condition Report

The RICS Condition Report is a basic overview survey. Use this if you’re buying an orthodox or new-build home in decent repair.

The report will identify any urgent defects, risks, condition and possible legal hold ups. This report will set you back around £250.

RICS HomeBuyer Report

The HomeBuyer Report goes a little further than the condition report. Again, it’s for run of the mill homes that seem in good repair.

The survey will uncover structural problems in- or outside the home. These are more serious ailments, like subsidence or damp. It won’t, however, dig under the floorboards or go beyond the brick- and plasterwork.

Some include a valuation. If the report values the property lower than expected, you may be able to negotiate the sale price down.

If not, you could still use any of the report’s findings to reduce the price. If there’s a damp problem, reduce the offer price by the amount it will cost to rid the house of the problem.

The HomeBuyer Report begins at around £400, but can easily pay for itself.

RICS Building Survey

Use the Building Survey if you’re planning to do work on your new home. Or if the property you’re buying has some age to it.

The survey is a step up from the HomeBuyer Report and rates any problems found. It also projects how serious any problems could get if left unaddressed.

This means you can prioritise what the problems and your tasks are at a glance. Plus, it will give you solid advice about methods to carry out the repairs.

The Report costs £400-£500, but gives you a solid platform from which to start.

RICS Building/Full Structural Survey

The Full Structural Survey is comprehensive. It does everything but check under the floorboards and behind walls. Older homes and those in some disrepair will benefit from this survey. But there’s no reason you can’t request one for any home.

Many contractors buy properties for Buy-to-Let purposes, often at auction. If the vendor hasn’t done this survey, it might be worth you doing one before raising your paddle.

The survey is more critical than the others and rarely includes a valuation. But the surveyor should summarise potential pitfalls and options to repair issues separately.

You can leverage any points against the sale price and bargain with your estate agent. Beginning at £600, the survey contains a reparation blueprint. It could be worth paying the fee to reach that starting point alone.

New-build snagging survey

Even new-build properties are not without fault, especially as they ‘settle’. This survey is independent from the developer, which is no bad thing. It will identify any potential problems with the property.

You have the right to request the developer correct the issues before you pick up your keys. This report will set you back around £300.

Should faults show after you move in, like plaster cracking, you have options. New builds often have a grace period where you can report developing problems to a site manager.

Any developer fixed ‘warranty’ period is separate from the RICS snagging survey. But the grace period gives you the opportunity to alert developers to new issues.

Haulage/moving costs

The last cost is the cost of moving if you’re a homemover or first-time buyer. Costs vary dramatically across the UK. Location, volume, timescale and distance between homes you’re moving to/from impact costs.

It’s worth shopping around to get comparisons. Check that your haulage firm has insurance, too. The cheapest might be the cheapest for a reason. You don’t want the surprise cost of replacing your furniture to blow your budget at the last minute.